India's Carbon Credit Trading Scheme (CCTS): What It Means for Your Business

Compliance & Regulations

PS Team

June 4, 2026

Table of Contents

India just crossed a significant milestone in its climate journey. The Carbon Credit Trading Scheme — better known as CCTS — is no longer something to plan for down the road. FY 2025–26 is the first compliance year, GHG intensity targets have been formally notified for all 8 covered sectors, and the clock is already running.

If your company operates in any of those sectors, this is live compliance — not future planning.

So what exactly is CCTS? How does it work? And what does your company actually need to do?

Let's break it down in simple language.

What Is the CCTS?

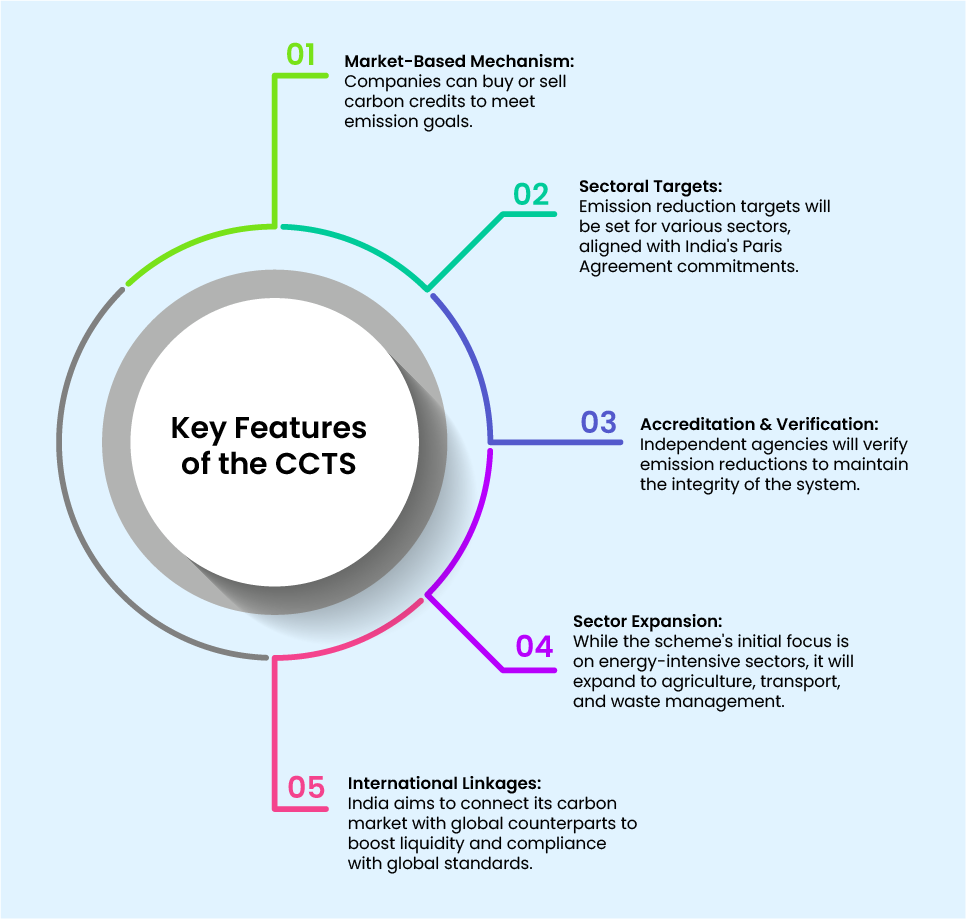

Think of CCTS as India's answer to carbon markets that have been running in Europe and China for years. The basic idea is straightforward: your industrial facility gets a GHG emissions intensity target. Perform better than that target, and you earn Carbon Credit Certificates (CCCs) that you can sell. Fall short, and you need to buy certificates from others to stay compliant.

The scheme measures performance in terms of Greenhouse Gas Emissions Intensity (GEI) — expressed as tonnes of CO₂ equivalent per unit of product output, not as an absolute cap on total emissions. That distinction matters. You can grow your production and still comply, as long as you're getting cleaner per unit.

The CCTS was established under the Energy Conservation (Amendment) Act, 2022, and formally notified on June 28, 2023. It represents India's transition from the Perform, Achieve and Trade (PAT) scheme — which focused on energy efficiency — to a comprehensive GHG emissions trading system aligned with India's Paris Agreement commitments.

Who Manages It?

Governance sits across three bodies. The Ministry of Power and the Ministry of Environment, Forest and Climate Change (MoEFCC) share policy oversight. The Bureau of Energy Efficiency (BEE) administers the scheme on the ground — setting targets, reviewing verification reports, and issuing Carbon Credit Certificates. Grid India operates the Indian Carbon Market (ICM) registry, which is where all CCCs are held and tracked.

The National Steering Committee for the Indian Carbon Market (NSC-ICM) plays a central role in recommending credit issuances and maintaining market integrity.

Which Sectors Are Covered?

Eight industrial sectors are currently covered under CCTS:

- Aluminium

- Cement

- Chlor-Alkali

- Pulp and Paper

- Iron and Steel

- Petroleum Refining

- Petrochemicals

- Textiles

GHG emissions intensity targets for all 8 sectors were formally notified via the GHG Emissions Intensity Target Rules 2025, published in the Gazette of India on October 8, 2025. These are facility-specific targets — each obligated entity has its own assigned benchmark, not a sector-wide number.

If your company operates in any of these industries, you are almost certainly in scope.

How Do the Targets Work?

Each obligated facility is assigned a GHG Emissions Intensity (GEI) target, expressed as tCO₂e per tonne of equivalent output. These targets are facility-specific, set against a baseline of FY 2023–24 actual performance, and tighten progressively — with FY 2025–26 as the first compliance year and further reductions required in FY 2026–27.

BEE has committed to notifying targets through 2030, creating a clear long-term trajectory.

This graduated approach is deliberate. The scheme doesn't demand a dramatic overnight shift. It's a ratchet — modest in year one, tightening over time — which is exactly why building the data and monitoring infrastructure now, rather than later, gives you the most room to manage your position strategically.

The Two Pillars: Compliance and Voluntary

CCTS operates through two distinct mechanisms under the Indian Carbon Market.

- The first is the Compliance Mechanism — mandatory for obligated entities. This is the one that applies to facilities in the 8 covered sectors with assigned GEI targets.

- The second is the Offset Mechanism — currently voluntary, and open to non-obligated entities who want to register GHG reduction projects and earn CCCs through the ICM.

Here's a critical point that's easy to miss: offset credits from the voluntary mechanism cannot be used to meet mandatory compliance obligations. The two pillars are completely separate. If your facility has a compliance obligation, you cannot buy voluntary offset credits and treat that as compliance.

How the Credit Cycle Actually Works

Here's the end-to-end flow, simplified.

Step 1 — You receive a target. BEE assigns your facility a facility-specific GEI benchmark based on your sector and FY 2023–24 baseline data.

Step 2 — You build a monitoring plan. Each obligated entity must develop a monitoring and reporting plan covering the methodologies, equipment, data collection frequency, and quality controls it will use to track GHG emissions. This plan must be submitted to BEE for approval. According to the CCTS detailed procedure, this submission is required within three months of the start of the first trajectory period.

Step 3 — You track and report emissions. At the end of the compliance year, you prepare a GHG emissions report. The detailed procedure requires submission within four months of year-end, along with verification by an accredited agency.

Step 4 — Independent verification. Your emissions report is audited by a Government-accredited Carbon Verification Agency (ACVA), accredited by BEE. These agencies check the reported data, your monitoring plan implementation, and your data management systems.

Step 5 — Credits are issued or a shortfall is recorded. If your facility's actual GEI came in below your target, you've outperformed. BEE issues the corresponding number of CCCs to your account on the ICM registry. The NSC-ICM makes its recommendation within two weeks of receiving the verified report; BEE issues within two weeks of that. If you fell short, you need to purchase and surrender the equivalent number of CCCs to cover the gap.

Step 6 — Trading and banking. Surplus CCCs can be sold on supervised power exchanges or held for future compliance periods. Banking is permitted — there is no expiry on issued CCCs. Borrowing against future allocations is not permitted.

What Happens If You Don't Comply?

Under the GHG Emissions Intensity Target Rules 2025, facilities that fail to surrender the required CCCs face an environmental compensation order imposed by the Central Pollution Control Board (CPCB). The compensation amount is equal to twice the average market price of CCC trading during that compliance year's trading cycle.

Payment must be made within 90 days of the order being imposed. Failure to pay triggers liability under the Environment Protection Act, 1986.

The 2× penalty is deliberately steep. It creates a strong incentive to start building your monitoring and compliance systems well ahead of submission deadlines — not in the final weeks before they're due.

Why This Matters Beyond India's Borders

If your company exports to Europe in steel, aluminium, cement, or petrochemicals, CCTS compliance carries an additional strategic dimension.

The EU's Carbon Border Adjustment Mechanism (CBAM) applies carbon costs to imports from countries without equivalent carbon pricing. Indian exporters in these sectors face direct exposure. CCTS participation — and the verified domestic carbon price it represents — could reduce that CBAM burden and protect export market access over time.

This means CCTS isn't just an Indian regulatory obligation. For export-facing businesses, it's a competitive variable worth tracking carefully.

How Is CCTS Different from PAT?

Many companies in these sectors have already been through PAT — the Perform, Achieve and Trade scheme. CCTS builds on that foundation but goes significantly further.

PAT tracked energy efficiency, expressed in energy savings, and used Energy Savings Certificates (ESCerts). CCTS tracks direct GHG emissions intensity across all greenhouse gases — not just energy-related CO₂ — and uses Carbon Credit Certificates that will trade on power exchanges.

The MRV requirements under CCTS are stricter. The market infrastructure is more formal. And unlike PAT, CCTS is explicitly designed to align with international carbon market standards — which has direct implications for CBAM and future cross-border trade.

If you've managed PAT compliance, you have a head start. But CCTS is a different exercise, and the data requirements are more demanding.

What Should Your Company Be Doing Right Now?

If you're in a covered sector, here is the practical preparedness checklist.

- Know your baseline. FY 2023–24 is the reference year for all GEI targets. You need accurate, facility-level Scope 1 emissions data for that year — broken down by fuel type, process emissions, and production output. If you don't have this in clean, auditable form, that's the first gap to close.

- Get your monitoring plan in order. This is a formal BEE submission, not an internal document. The systems and data processes you put in place now will determine the reliability of your verified reports at year-end.

- Understand your facility-level GEI target. Your specific target is published in the GHG Emissions Intensity Target Rules 2025 gazette. Know where your facility stands against that number today — are you likely to outperform and earn credits, or do you need to plan for a shortfall?

- Prepare for third-party verification. Every emissions report gets audited by a BEE-accredited verification agency. The data trail behind your numbers — meter readings, calculation methodologies, monitoring equipment records — needs to hold up under independent scrutiny.

- Think about credit strategy early. If your facility is tracking ahead of its target, the CCCs you earn are a financial asset. If you're tracking behind, understanding your credit procurement options before year-end gives you time and negotiating room. Either way, this is a CFO-level conversation, not just a sustainability team conversation.

This is exactly where Karbon comes in. Accurate, audit-ready GHG data across your facilities — structured to support BRSR reporting, CCTS monitoring plans, and third-party verification — is not something you want to be assembling manually in a spreadsheet under a four-month deadline.

Frequently Asked Questions

- What is CCTS in India?

- The Carbon Credit Trading Scheme (CCTS) is India's mandatory GHG emissions trading system for heavy industrial sectors, established under the Energy Conservation (Amendment) Act, 2022 and notified on June 28, 2023. Obligated facilities must meet facility-specific GHG emissions intensity targets. Those that outperform earn tradeable Carbon Credit Certificates; those that fall short must purchase them.

- Which industries are covered under CCTS?

- Eight sectors: Aluminium, Cement, Chlor-Alkali, Pulp and Paper, Iron and Steel, Petroleum Refining, Petrochemicals, and Textiles. Facility-specific GEI targets for all 8 sectors were notified via the GHG Emissions Intensity Target Rules 2025 (Gazette of India, October 8, 2025).

- What is the first compliance year for CCTS?

- FY 2025–26 is the first compliance year. Targets use FY 2023–24 as the baseline and tighten progressively through FY 2026–27 and beyond, with BEE committed to notifying targets through 2030.

- What is a Carbon Credit Certificate (CCC)?

- A CCC represents a reduction of one tonne of CO₂ equivalent (tCO₂e). Facilities that reduce their GHG emissions intensity below their assigned target receive CCCs, which can be traded on supervised power exchanges or banked for future compliance periods.

- Can a company use voluntary carbon offsets for CCTS compliance?

- No. The voluntary offset mechanism under CCTS is entirely separate from the compliance mechanism. Offset credits cannot be used to meet mandatory compliance obligations.

- What is the penalty for non-compliance?

- Under the GHG Emissions Intensity Target Rules 2025, the Central Pollution Control Board (CPCB) imposes an environmental compensation equal to twice the average CCC market price for that compliance year. Payment is due within 90 days of the order.

- How is CCTS different from the PAT scheme?

- PAT tracked energy efficiency using Energy Savings Certificates (ESCerts). CCTS targets direct GHG emissions intensity across all greenhouse gases, applies stricter MRV requirements, and is designed to align with international carbon market standards — including potential relevance to EU CBAM for Indian exporters.

- How does CCTS connect to BRSR reporting?

- Both frameworks require accurate facility-level GHG data. BRSR Core already mandates GHG intensity reporting for India's top listed companies. The Scope 1 and Scope 2 emissions tracking infrastructure built for BRSR is the same foundation needed for CCTS monitoring plans and verified annual reporting.