BRSR Reporting Made Simple: Essential Guide for Top 1,000 Listed Entities

Compliance & Regulations

PS Team

January 21, 2026

Table of Contents

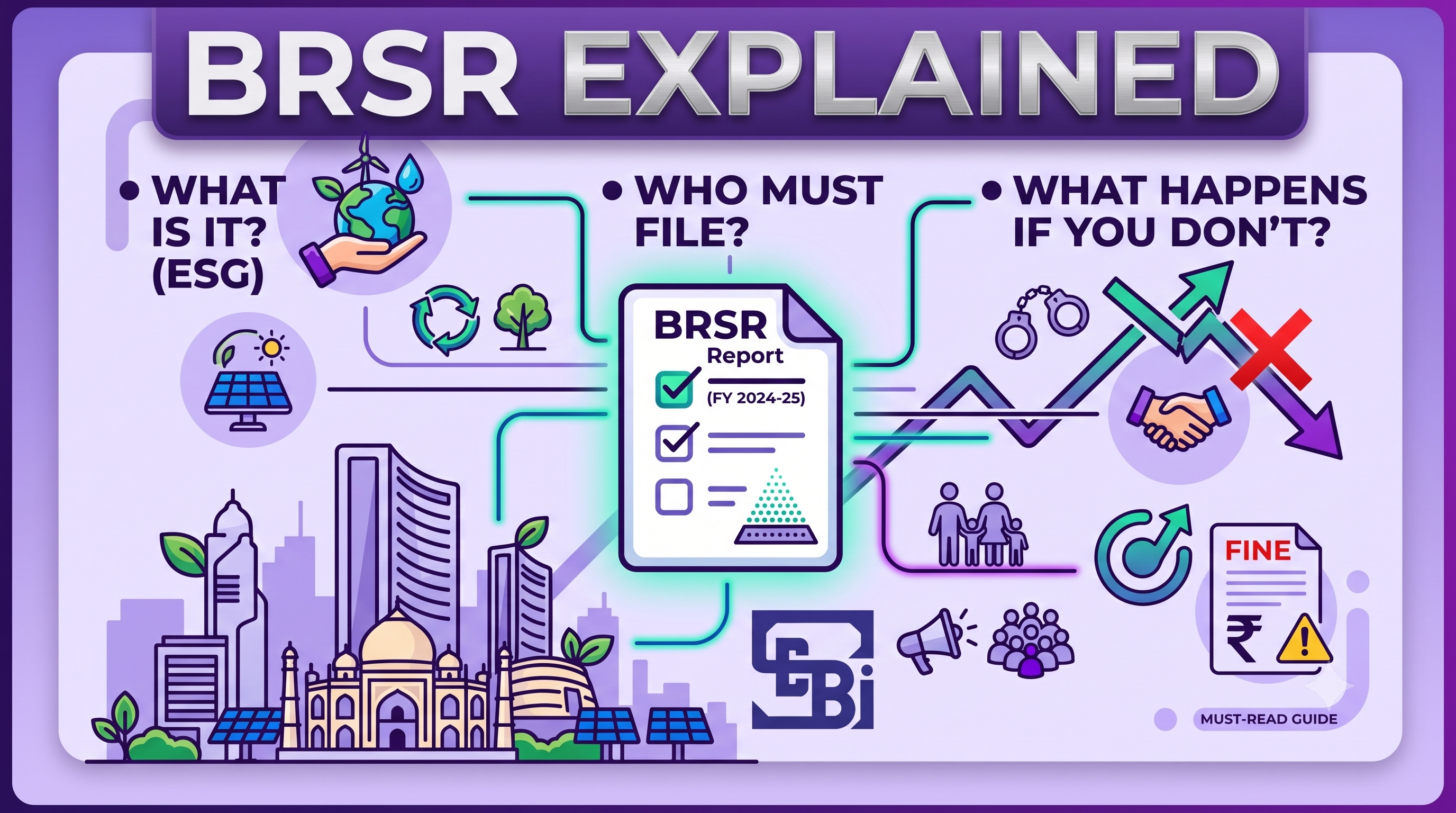

Business Responsibility and Sustainability Reporting (BRSR) has become a key regulatory requirement for Indian companies as sustainability reporting moves from voluntary disclosure to structured compliance. Mandated by SEBI for the top 1,000 listed entities, BRSR provides a standardized framework for reporting environmental, social, and governance (ESG) performance.

For organizations preparing for BRSR reporting, the real challenge lies in data readiness, cross-functional coordination, and process maturity. This guide explains how companies can prepare for BRSR effectively and build a scalable reporting process.

Understanding BRSR: SEBI's Mandatory ESG Framework

BRSR is based on SEBI’s National Guidelines on Responsible Business Conduct (NGRBC) and is structured around nine principles covering areas such as ethics, employee welfare, environmental impact, value chain responsibility, and consumer protection.

BRSR reporting helps companies:

- Meet SEBI compliance requirements

- Improve ESG transparency for investors

- Strengthen internal governance and risk management

- Align sustainability efforts with business strategy

Step 1: Map Your BRSR Applicability (Core vs. Standard)

Before starting BRSR preparation, companies must clearly understand:

- Whether BRSR or BRSR Core is applicable

- Mandatory vs voluntary indicators

- Quantitative and qualitative disclosure requirements

Not all indicators require the same level of effort. Early clarity helps prioritize high-impact and data-intensive disclosures.

Step 2: Perform a Data Readiness Gap Analysis

A BRSR gap assessment identifies the difference between current data availability and BRSR disclosure requirements.

Key questions to address:

- What ESG data already exists within the organization?

- Is the data aligned with BRSR definitions and formats?

- Which indicators lack reliable data sources?

Most first-time reporters find that a large portion of required data exists but is not structured for BRSR reporting. A gap assessment helps define timelines, responsibilities, and system requirements.

Step 3: Establish Governance and Data Ownership

BRSR reporting requires inputs from multiple departments, including HR, EHS, Finance, Legal, Procurement, and Operations.

Best practices include:

- Appointing a central BRSR or ESG owner

- Assigning indicator-level data owners

- Defining review and approval workflows

Strong governance ensures accountability, data accuracy, and audit readiness — especially important for companies covered under BRSR Core.

Step 4: Standardize Definitions and Methodologies

Inconsistent interpretation is a common risk in BRSR compliance.

Organizations should document:

- Definitions for employees, workers, and contractors

- Methodologies for energy, emissions, water, and waste

- Calculation logic and reporting boundaries

Creating a BRSR data dictionary improves year-on-year consistency and supports third-party assurance requirements.

Step 5: Build Your BRSR Data Collection System

Manual data collection through emails and spreadsheets increases the risk of errors.

An effective BRSR data collection process includes:

- A fixed annual reporting calendar

- Standardized templates aligned with BRSR indicators

- Internal validation checks

- Supporting documents and evidence

As reporting matures, many organizations adopt ESG or BRSR software platforms to centralize data and improve traceability.

Step 6: Prioritize Environmental Data for BRSR

Environmental disclosures typically require the most effort during BRSR preparation.

Key environmental metrics include:

- Energy consumption and renewable energy usage

- Scope 1 and Scope 2 greenhouse gas emissions

- Water withdrawal, consumption, and discharge

- Waste generation and disposal

Where exact data is unavailable, companies should use reasonable estimates with documented assumptions and improve data quality over time.

Step 7: Prepare for BRSR Core and Assurance Requirements

Companies falling under BRSR Core face additional requirements such as:

- Enhanced quantitative disclosures

- Greater focus on value-chain ESG data

- Mandatory third-party assurance

Early preparation, supplier engagement, and strong internal controls are essential to meet these expectations efficiently.

Step 8: Draft Clear and Consistent Narrative Disclosures

BRSR reporting is not limited to numbers. Narrative disclosures explain policies, processes, and outcomes.

Effective narratives:

- Reflect actual practices

- Align with quantitative data

- Clearly state improvement plans

Avoid generic or exaggerated claims, as ESG disclosures are increasingly scrutinized for greenwashing risks.

Step 9: Establish BRSR as an Ongoing ESG Program

Successful organizations treat BRSR as an ongoing journey:

- Year 1: Achieve baseline BRSR compliance

- Year 2: Improve data quality and coverage

- Year 3: Integrate ESG insights into strategic decisions

Post-report reviews help identify gaps, improve efficiency, and strengthen future disclosures.

Conclusion

BRSR reporting marks a significant shift in ESG compliance in India. While the first reporting cycle can be complex, companies that invest in governance, data systems, and standardized processes find that BRSR becomes easier and more valuable each year.

By approaching BRSR preparation strategically, organizations can not only meet SEBI requirements but also enhance transparency, resilience, and long-term stakeholder trust.

Schedule a Consultation: BRSR Preparation Support